Carla Nunes

Managing Director

Valuation Advisory Services

Philadelphia

Wed, Feb 14, 2024

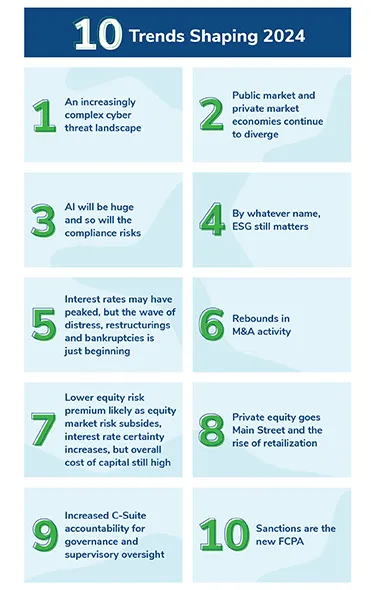

Against a global backdrop of intense geopolitical uncertainty, highly contentious elections in the U.S. and around the world, diverging economic trends and evolving regulatory imperatives, 2024 is poised to be a year of both heightened risks and opportunities. Kroll experts share ten major trends that are shaping financial markets, the regulatory and governance environment, compliance and cybersecurity. For businesses and investors alike, the key themes we are monitoring revolve around navigating complexity, embracing uncertainty and emphasizing the importance of vigilance and accountability.

In an ever-evolving cyber threat landscape, expect enhanced use of artificial intelligence (AI) both in cyberattacks and defense, increasing attacks on software supply chains – and more sophisticated and targeted Ransomware attacks. Threat actors will continue to exploit Zero-Day and One-Day vulnerabilities and target remote workers and associated infrastructure. Business Email Compromise (BEC) will continue to pose a threat to all organizations and cloud security will become increasingly complex as more organizations move to cloud-based solutions. Regulatory compliance and data privacy will only grow in importance. With so many focus areas for risk, the need for vigilance and effective cybersecurity strategies is greater than ever.

Learn more: Case Study: Office 365 BEC Investigation, 2024 Cyber Horizon

Public equity valuations in the U.S. and in some European markets have hit record highs and corporate profits remain at historically elevated levels. The global economy surprised most forecasters on the upside during 2023, thanks in part to the resilience in the U.S. and a rapid decline in energy prices globally. While 2024 overall global growth is expected to slow down, a dual track seems to be emerging, with certain Asian markets in the driver’s seat and advanced economies stumbling along.

Amidst this backdrop, a riptide economy lurks just below the surface in the massive, but less visible private market segment that is still highly over-levered. That foreshadows more restructurings ahead and value resets that could create significant economic ripples, with commercial real estate among the most vulnerable sectors. Election-year political turbulence and market volatility factors only add to the uncertainty, underscoring the importance of effectively navigating complexity and the imperative of quality information, particularly around diligence and valuation.

Learn more: Valuation Outlook Insights

The rapid emergence of artificial intelligence is likely to accelerate with a profound impact across sectors. AI will be a crucial tool in risk management, helping to detect and prevent issues and problems, from cybercrimes to financial irregularities, while posing its own set of risks. Regulators are scrambling to keep up. The European Union’s preliminary agreement on comprehensive AI regulation and the SEC’s initial proposed AI-related rules are just the tip of the iceberg of imminent regulatory changes. Unmitigated and uncontrolled AI risks could expose investment advisers and financial services providers to reputational, enforcement and examination liability across a broad range of regulatory concerns around AI. CCOs and compliance officers need to take steps now to understand AI risks and how to mitigate the risk of noncompliance when adopting AI tools into workplace operations.

Learn more: AI Risks and Compliance Strategies

While Environmental, Social & Governance (ESG) has become a politically contentious buzzword, especially in the U.S., the regulatory impetus around increased ESG disclosure and regulation remains strong. In the U.S., the SEC is reluctant to cede the regulatory framework entirely to EU rulemaking while in the EU, the European Commission and ESMA continue to advance ESG-focused regulation and requirements. In Latin America, multiple countries are seeking to regulate the region’s carbon markets and in Asia Pacific, reporting requirements and regulations around ESG factors are being enhanced.

The new requirements from the International Valuation Standard Councils (IVSC) and the International Sustainability Standards Board (ISSB) are expected to impact businesses globally, which will add complexity and the need for coordination with several country-specific requirements. As they navigate the political controversy, companies and funds will have to deal with ESG considerations, from rules against greenwashing and conflicting investor demands to new financial reporting requirements and compliance, as enforcement is stepped up and litigation rises. At the same time, significant investment will flow to energy transition vehicles and green financing, creating opportunities for companies and investors well positioned to take advantage of tax and other related incentives.

Learn more: ESG and Global Investor Returns Study, Challenges with ESG Reporting and Transparency

After the Federal Reserve raised interest rates aggressively in 2022 and 2023 to curb inflation, financial markets are currently predicting significant rate cuts for 2024. While rates have likely reached their peak, the Fed will exercise caution with timing and pace to prevent a premature reduction that could reignite inflation. Central banks in the UK and Eurozone are following suit.

Even with some rate cuts, if interest rates remain elevated for an extended period, 2024 is likely to see increased restructuring activity. With a significant volume of debt maturing in the near term, more companies will need to re-optimize their capital structures to raise new liquidity and deleverage, leading to a fair amount of distress – particularly in the highly-levered segments of the market. If restructurings/refinancings cannot be achieved consensually, activity will likely be facilitated through greater use of the bankruptcy process. Even as overall market conditions improve, expect to see more debt restructuring, forced sales and Chapter 11 filings.

Learn more: Restructuring Insights

Expectations that interest rates have peaked and will come down in 2024 have significantly improved the outlook for M&A in the U.S. M&A activity and optimism have also improved in Asia Pacific and Europe. Private equity firms that have largely been on the sidelines as interest rates rose and are behind on distributed to paid-in capital (DPI) ratios are likely to be more aggressive in deploying capital and harvesting investments to return capital to their limited partners.

Combine that with strategic buyers who remain well-capitalized, hold substantial cash balances and maintain a keen interest in synergistic acquisitions, and the outcome will be a much more robust M&A marketplace. Returns that will ultimately be realized are likely to be lower than in previous years, particularly due to higher borrowing rates. With returns compressed, managers’ valuation marks are likely to be meticulously assessed and scrutinized. Exit opportunities continue to be a challenge, with IPO markets slower to pick up and investors focused on those companies with more robust prospects of profitability.

Learn more: M&A Insights

Interest rates and the cost of capital remain significantly higher than immediately following the outbreak of COVID-19. Recently, as interest rate uncertainty subsided and the scenario of a soft landing became plausible, investor confidence has risen.

While markets may still experience a roller-coaster ride while waiting for interest rates to settle, continued strength in consumer spending and job markets, coupled with an expected improvement in earnings growth, will lead equity markets to test new highs. This risk-on attitude means the equity risk premium is likely to come down. Even if interest rates stay higher for longer than some anticipate, greater certainty on the interest rate outlook may translate into a lower equity risk premium. Nevertheless, a scenario of ultra-low interest rates is not in the cards for 2024, and overall cost of capital is likely to stay high.

Learn more: The New Normal: Cost of Capital in a Higher-Interest-Rate Environment, Recommended Equity Risk Premium and Corresponding Risk Free Rates

Previously reserved for ultra-high net worth investors, private equity and other alternative investments are now more accessible to retail investors. This is facilitated by the expanded use of 40 ACT funds, which are even finding their way into the self-directed 401K plans of qualified investors. From a disclosure and reporting perspective, this signifies a complete change in thinking. Instead of reviewing information quarterly, which is often significantly delayed, it’s now monitored monthly or even daily, providing real-time insights.

This means not only greater emphasis and rigor around quarterly reporting but also the need for greater rigor around valuation underpinning that reporting, as reflected in significant regulatory changes, such as the SEC’s new rules on private fund advisors and fairness opinions for private equity continuation funds. While retailization has been more of a U.S. phenomenon, its implications are global as the influx of retail funds into private equity subjects the entire industry to greater scrutiny. In Asia Pacific financial hubs, there is increased scrutiny from regulators, boards and limited partners on valuation of investments by alternative investment funds. The result is likely to be a need for more timely and more frequent valuation or fairness opinions and an even greater emphasis on governance.

Learn more: When and How Will Private Investment Structures Find Their Way to Mainstreet?, Outlook shaping alternative asset valuation, Twenty–Three Potential Compliance Pitfalls in the SEC’s New Private Fund Rules

Traditionally, on matters related to corporate governance and oversight, the SEC directed much of its activities and communications to chief compliance officers. That is changing and the SEC is increasingly directing its messaging and actions to the upper ranks of the c-suite to not only increase accountability, but also ensure that compliance is fully and properly resourced both in terms of human capital and systems. For CEOs and other principals, plausible deniability when it comes to compliance issues is no longer an option.

Learn more: Thirteen Questions Every CEO of an SEC-Registered Entity Should Ask

While in past years violations of the Foreign Corrupt Practices Act (FCPA) garnered a lion’s share of attention and penalties, in the current geopolitical environment, sanctions evasion is increasingly likely to be the focus of criminal and civil prosecutors.

Recent history shows that the use of sanctions and export restrictions transcends Administrations and has only intensified since the War in Ukraine. Corporations that are noncompliant face immense financial and reputational consequences. In an ever-changing environment, navigating the complex world of sanctions compliance is a significant challenge for multinational corporations with immense potential financial and reputational risks.

Learn more: The Future of Sanctions Compliance Programs: Navigating the Challenges of a Complex Global Landscape

Valuation of businesses, assets and alternative investments for financial reporting, tax and other purposes.

End-to-end governance, advisory and monitorship solutions to detect, mitigate and remediate security, legal, compliance and regulatory risk.

Middle Market M&A, Strategic Advisory, Debt Advisory and Private Capital Markets, Restructuring and Insolvency Services, Financial Due Diligence, Fairness Opinions, Solvency Opinions and ESOP/ERISA Advisory.

Incident response, digital forensics, breach notification, security strategy, managed security services, discovery solutions, security transformation.

Advisory and technology solutions, including policies and procedures, screening and due diligence, disclosures and reporting and investigations, value creation, and monitoring.

World-wide expert services and tech-enabled advisory through all stages of diligence, forensic investigation, litigation, disputes and testimony.